The Worrying Trend of Small Business Owners Trying to Turn to Overdrafts

Since the covid pandemic, a worrying trend that has been highlighted is that many small business owners are trying to turn to bank overdraft facilities more and more often as a way of securing additional funding at a time when the traditional overdraft is becoming as common as a rainbow unicorn.

In this post, we’ll discuss the reasons why small businesses are thinking of using overdrafts and also look at some of the alternatives available.

What Is a Bank Business Overdraft?

A business bank overdraft is an arranged credit facility with a bank. This means that the business can spend up to a certain limit beyond their account’s zero balance. The limit amount, the interest rate, and any other fees and security required will be agreed upon between the business and their bank when the overdraft is discussed.

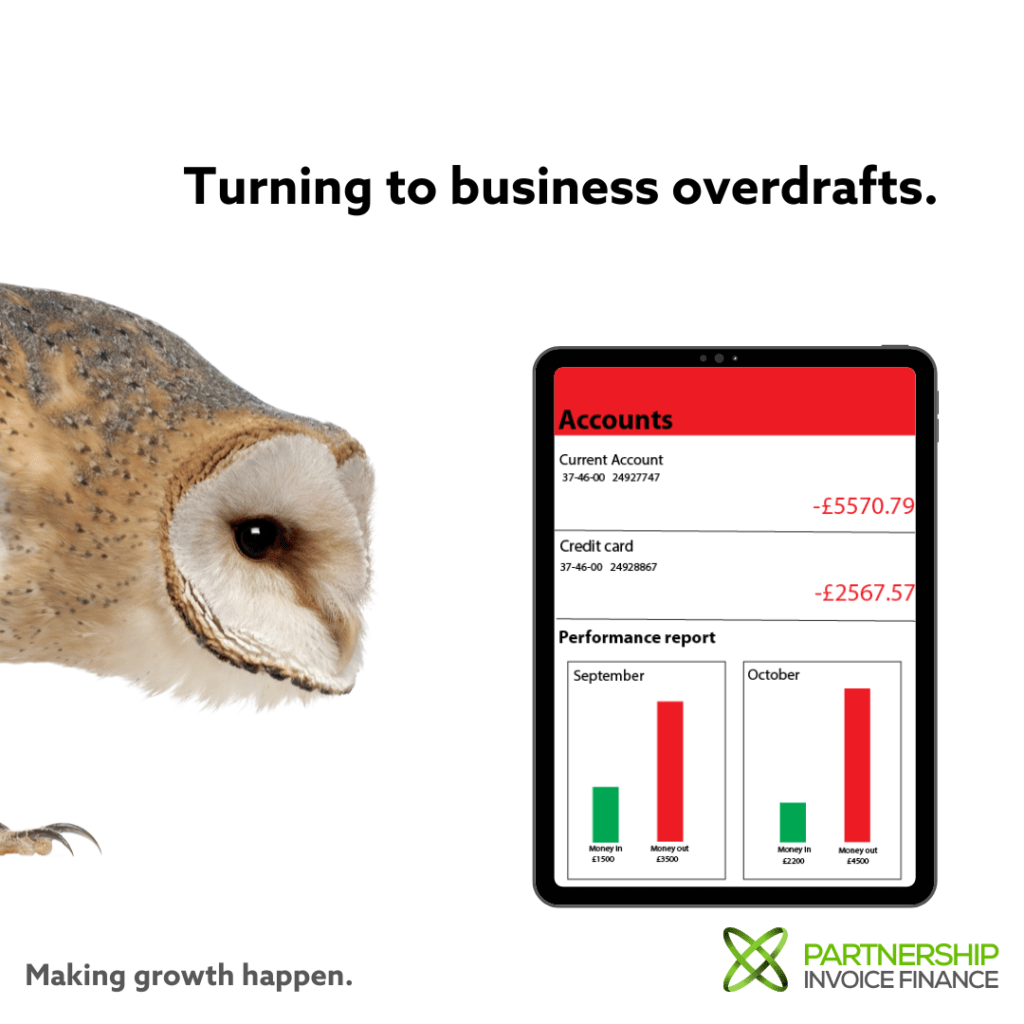

Business overdraft facilities are often in place to be used in case of an emergency, and seasonal or short-term cash flow issues which themselves are often caused by the need to pay bills before being paid. It is not designed to be used long-term or to purchase capital equipment.

Why Are Small Business Owners Using Their Overdraft Facility More Often?

There are various reasons why small businesses may decide to use an overdraft facility, these can include:

Covering unexpected costs – Many small businesses don’t have a large amount of spare cash available to cover unexpected costs, such as an unforeseen repair bill.

Expanding the business – When a business starts to grow and expand more cash is generally needed until such time as additional profit can be made and retained in the business. It may not have the necessary funds available, finding it difficult to obtain loans, and therefore, may look into using an overdraft to help with this.

Covering late payments – Small businesses may use their overdraft facility if they have customers who are regularly paying late or even if they just have to provide credit terms. This can cause cash flow problems for the business and so using an overdraft can help to bridge the gap.

Economic uncertainty – In times of economic uncertainty, small businesses may be more likely to use their overdraft facility or try to arrange one as a safety net in case they experience any unforeseen problems.

Repayment of government-backed loans during Covid – Many small businesses have had to rely on their overdraft facility to meet the monthly payments now due under the government-backed loans issued to them during the Covid pandemic. This is a worrying trend as it shows that many small businesses are still struggling to stay afloat.

Lack of information about other funding sources – Another reason for this trend is that many small business owners simply don’t know where to get reliable additional funding from other than their current bank or feel that they don’t have the time to look into other options.

The Risks and Disadvantages of Regularly Using Your Business Overdraft Facility.

It’s important for small businesses to be aware of the risks of using an overdraft before they decide to use it. The main risks are:

Becoming reliant on the overdraft facility – Many small businesses become so reliant on their overdraft that they are in constant debt and struggling to repay what they have borrowed. This can put a lot of financial strain on the business and its owners.

High-interest rates – One of the main drawbacks of using an overdraft is that you will usually be charged high-interest rates. This can be even higher if you go over your agreed overdraft limit. The high-interest rates on overdrafts can cost small businesses dearly. The associated costs can quickly add up, meaning that businesses can end up paying a lot more for the money they borrow.

More effective Funding Sources are Available.

Too often an overdraft is turned to as a catch-all when finance is required as opposed to looking at finance specific to the business needs, so it’s important for small businesses to explore all their options before resorting to an overdraft. Other funding alternatives to an overdraft include:

Asset finance – Businesses use their assets, such as equipment or machinery, as security against a loan.

Business credit cards – Not really recommended for anything other than “emergency funds” but generally easy to obtain, these can be useful but often come with penal interest charges.

Grants and government support – There are various grants and government schemes available to help small businesses with funding, so it’s worth checking what’s available in your area.

Factoring and invoice financing – Businesses can get access to funding by selling their invoices to a third party at a discount, in order to get the money, they’re owed immediately, rather than waiting for payment.

What Is Invoice Finance?

Invoice finance is a type of funding that allows businesses to access the cash tied up in their unpaid invoices. It works by businesses selling their outstanding invoices to a lender at a discount. The lender then pays the business an advance of up to 90% of the value of the invoice, with the remaining balance (less the lender’s fee) paid when the customer pays the invoice in full.

Invoice finance is a viable alternative to traditional business loans. If your business is struggling to secure finance from traditional lenders, invoice finance could be the perfect solution.

Invoice Finance benefits include:

- Access to cash quickly.

- No need to wait 30, 60, 90 days or more for customers to pay.

- The ability to free up time spent chasing late payments.

- Improve your business cash flow and working capital.

- Easy to access with a straightforward and short application process.

- Flexible, you choose which customers you want to factor.

- A facility that grows as you grow.

If your small business is regularly going into your business overdraft, then contact us about the invoice finance options we have available. At Partnership Invoice Finance we understand that small businesses often need access to quick and reliable funding, which is why we offer a range of Invoice Finance solutions.